The pattern that should not surprise anyone

A real estate sponsor tokenizes their fund. Mint goes well. The launch lands. The first wave of investors come in — friends, existing LPs, a handful of crypto-native participants who saw the announcement.

Then month two slows down.

By month three, the secondary market is dead, the primary raise has stalled at maybe 30–40% of target, and the sponsor is calling around asking what went wrong. The token works. The smart contract executes. The compliance is fine. Nothing is technically broken.

But nothing is moving either.

After eight years building tokenization infrastructure, $300M+ tokenized, and 100+ issuances across real estate, private credit, and other asset classes, the failure mode is consistent. It is structural — and it almost always traces to three specific decisions made or skipped before mint.

For more context on how real estate tokenization works in practice, see the complete real estate tokenization guide and real estate tokenization case studies.

Quick test: If your fund is launched and inflow is slowing, run Stobox Compass right now. Three minutes. The diagnostic identifies which of the three causes below is your specific problem, so you fix the right one — not all three at once.

The composite case

Consider a $40M tokenized real estate fund. EU jurisdiction. Mixed-use commercial portfolio. Sponsor has a strong direct-investment track record, new to tokenization. Picks a tokenization platform on a competitive RFP, sees a clean demo, signs.

Mint happens on schedule. Launch post performs well. First two weeks, $4.2M comes in — mostly existing LPs migrating on-chain.

Week five: inflow drops 70%. Week eight: broker-dealers the sponsor expected to distribute the offering aren't responding to outreach. Week ten: two early investors try to exit on the secondary market and find no bid. They escalate. Week twelve: the sponsor is on a call with the Stobox team asking what to do.

This is the script. The numbers vary. The pattern doesn't. And in nearly every case, the failure has the same three roots.

Fix 1 — The wrapper was wrong for the investor base they wanted to reach

The sponsor in this scenario set up the fund as a Cayman SPC with tokens issued as ordinary participating shares, sold under a Reg S exemption to non-US investors only.

That decision looked clean on paper. Cayman is familiar to fund managers. Reg S is straightforward. The token contract enforced the non-US-only restriction at every transfer.

But the sponsor's existing LP network was 60% US-based.

Those LPs could not legally hold the token. The migration narrative — "we'll bring our existing investors on-chain" — was structurally impossible from day one. Nobody flagged it in the structuring conversation because nobody asked the right question early enough.

The fix: A dual-track structure. Reg D 506(c) for US accredited investors, Reg S for non-US, with the token contract enforcing the eligibility split automatically using investor credentials at the wallet level. The wrapper itself can stay flexible — Cayman SPC works, but a Delaware LP feeder might be better depending on the LP base — but the exemption strategy has to match the investor base you actually intend to reach.

This is not a post-mint fix. Once the token is issued under one exemption, retrofitting a second exemption requires either issuing a parallel token class or restructuring the entire offering. Both options cost three to four months and significant legal work.

The lesson: Wrapper and exemption are two separate decisions, made together, calibrated to the actual investor base — not the imagined one.

Fix 2 — The transfer-restriction logic blocked the brokers they needed

The sponsor's token contract enforced a 12-month lockup post-issuance per Reg D / Reg S restricted-period requirements. Standard.

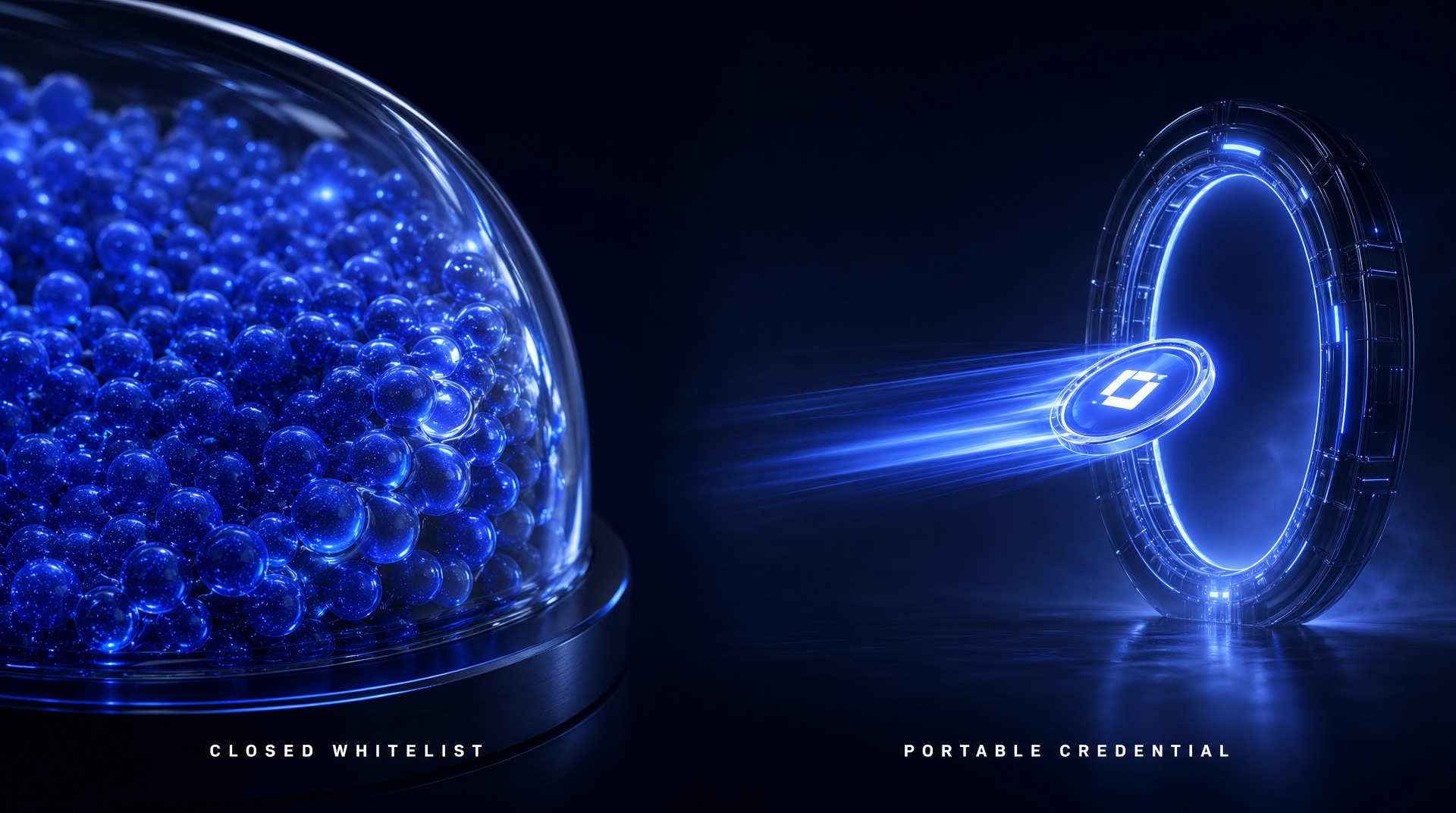

What was not standard was the secondary-transfer logic after lockup. The contract required every secondary transfer to verify the receiving wallet against a whitelist maintained by the platform vendor. Whitelisting required investors to onboard to the vendor's KYC system specifically. The vendor charged a platform fee per investor onboarded.

Brokers and placement agents the sponsor wanted to work with already had their own investor bases — onboarded to their own KYC systems, sitting on their own wallets, ready to transact.

But none of those investors were on the platform vendor's whitelist. To buy the token, they would have to onboard to a system they had no other reason to use, paying a fee for the privilege.

Most brokers walked.

The fix: Token contracts that enforce eligibility based on portable, verifiable credentials — not vendor-specific whitelists. Stobox tokens issued via Stobox STV3 use Stobox DID, which means an investor verified once carries that credential to any Stobox-issued asset and any participating broker. Stobox does not lock issuers into a closed onboarding moat. The broker's existing investors can transact in Stobox-issued tokens because the credential travels with the investor, not the platform.

If you are evaluating tokenization vendors, ask this directly: "Can a broker's existing onboarded investors transact in this token without re-doing KYC on your platform?"

If the answer is no, the vendor's economics depend on locking investors into their funnel. That is a problem for you, because brokers do not want to be in someone else's funnel either.

The lesson: The token contract is not just about compliance. It is about who can transact. Closed whitelists kill secondary liquidity. Portable credentials enable it.

Where do you stand on Fix 1 and Fix 2? Run Stobox Compass — the diagnostic flags wrapper / exemption mismatches and closed-whitelist transfer issues automatically.

Fix 3 — There was no distribution plan before mint

This is the big one.

The sponsor in this scenario assumed tokenization itself would produce distribution. That a launch announcement, some LinkedIn posts, and listing on a "tokenized assets marketplace" would result in inflow.

It does not. Not in 2026. Not before. Not for any tokenization project that has actually succeeded.

Tokenized real estate is not a consumer product. The investor base is institutional, accredited, qualified-purchaser-tier. They do not discover tokenized funds through marketplaces. They are reached through brokers, placement agents, RIA networks, family-office channels, and direct sponsor relationships — the same way every private placement has been distributed for thirty years. Tokenization changes the rail, not the surface.

The sponsor in this scenario had no broker relationships configured before mint. No placement agent agreement. No RIA channel. The plan was we will figure it out post-launch. Post-launch, brokers asked questions about wrapper, exemption, transfer logic — and the answers (see Fix 1 and Fix 2) made the offering hard to distribute.

By the time the structural issues were fixable, the sponsor had burned three months of the raise window and most of the goodwill with the brokers who had taken the first call.

The fix: Configure distribution channels before mint, not after. This means:

- Identifying 3–5 placement agents or broker-dealers whose mandate matches your asset class, before structuring is locked

- Sharing the proposed structure with them and getting their feedback on what they can and cannot distribute

- Adjusting the structure if their feedback identifies a gap (much cheaper to adjust pre-mint than post-mint)

- For Stobox issuers, opting into the Stobox broker network — vetted partners who already transact in tokenized real-world assets and underwrite Stobox-issued tokens because the structuring has been done to a standard they trust

The Stobox + tZERO infrastructure alignment is one example of how primary issuance and regulated secondary-market venues connect — see the partnership announcement.

The lesson: Distribution is a Day -30 problem, not a Day 30 problem. Configure it before mint or accept that you are launching into a vacuum.

What stalled funds can actually do

If your tokenized fund is in month two or three with the inflow curve flattening, here is the honest sequence:

1. Audit the structure. Independent review of wrapper, exemption, and transfer logic against the investor base you are actually trying to reach. One-week exercise with the right counsel and tokenization advisor. Tells you whether the gaps are fixable in-place or require rework.

2. Audit the token contract. Specifically: can a broker's existing investor base transact without re-doing KYC on a vendor-specific whitelist? If no, this is a meaningful drag on distribution and may need to be addressed before any broker conversation moves forward.

3. Configure distribution properly, late. Identify the 3–5 placement agents or brokers whose mandate fits your asset class. Be honest about where the offering sits. The ones who walk away because of structural issues are giving you the data you need. The ones who engage will tell you what to fix.

4. Run a readiness check before doing any of the above. Same diagnostic Stobox runs on every engagement, built into Compass — free, three minutes, eight questions. It tells you which of the three fixes is actually your problem, before you spend money fixing the wrong one.

The sponsors who recover from a stalled month-three issuance are the ones who diagnose accurately and fix structurally. The ones who do not recover are the ones who add more marketing on top of a broken foundation, run another launch post, and assume volume will come back.

It does not.

The pattern, summarized

| Fix | Cause | Pre-mint cost to fix | Post-mint cost to fix |

|---|---|---|---|

| Fix 1 | Wrapper / exemption mismatched to investor base | 1–2 weeks legal work | 3–4 months restructuring or parallel token class |

| Fix 2 | Closed-whitelist transfer logic blocks brokers | 1 week vendor selection | Re-mint required if vendor cannot adjust |

| Fix 3 | No pre-mint distribution plan | 2–4 weeks broker outreach | 4–6 months building distribution from scratch |

Tokenization fails at distribution, not at the smart contract. All three failure modes above are addressable before mint. Two of three are very expensive to fix after mint. The third — distribution — is fixable late but eats months of runway in the process.

Frequently asked questions

Before you spend another week

If you are about to tokenize a real estate fund, run the readiness check first.

If your fund is already stalled, run the readiness check now to identify which of the three fixes is your actual problem. Then fix that one — not the other two.

Run your free readiness assessment on Stobox Compass →

Eight questions. Three minutes. The same diagnostic Stobox runs on every client engagement — now free, public, no signup required.

Open Stobox Compass →