Welcome to the Stobox Weekly RWA & Tokenization Digest — the briefing that tells busy operators what actually changed in real-world asset tokenization, and what to do about it.

This was not a quiet week. In seven days, tokenized securities moved from theory to production inside the US regulatory perimeter, the largest tokenization infrastructure firm became a public company on the New York Stock Exchange, and Europe’s crypto market crossed a hard legal line into licensed-only operation. The through-line: tokenization stopped being a pilot story and became a market-structure story. The people building capital-markets plumbing — clearinghouses, transfer agents, transfer networks — are now the ones shipping.

Below are the ten developments that matter most, each with our read on the consequences. Facts first, then interpretation.

This week in one minute

- Ondo Finance launched the first US custodial tokenized securities — tokenized BlackRock IVV and Micron shares that carry full shareholder rights, with proxy voting handled by Broadridge.

- Securitize began trading on the NYSE under the ticker SECZ after a Cantor SPAC merger that raised roughly $400M.

- Ripple received full MiCA authorization in Luxembourg, passporting regulated crypto and stablecoin services across all 30 EEA countries.

- MiCA’s transitional period ended on July 1 — the EU is now a licensed-only market, and roughly 283 of about 1,200 firms made it through.

- JPMorgan’s tokenized money-market fund roughly doubled to about $693M, pulled up by stablecoin reserves seeking on-chain yield under the GENIUS Act.

- Total tokenized RWA sits near $33.5B in liquid on-chain value — and closer to $60B if you count permissioned and dormant products.

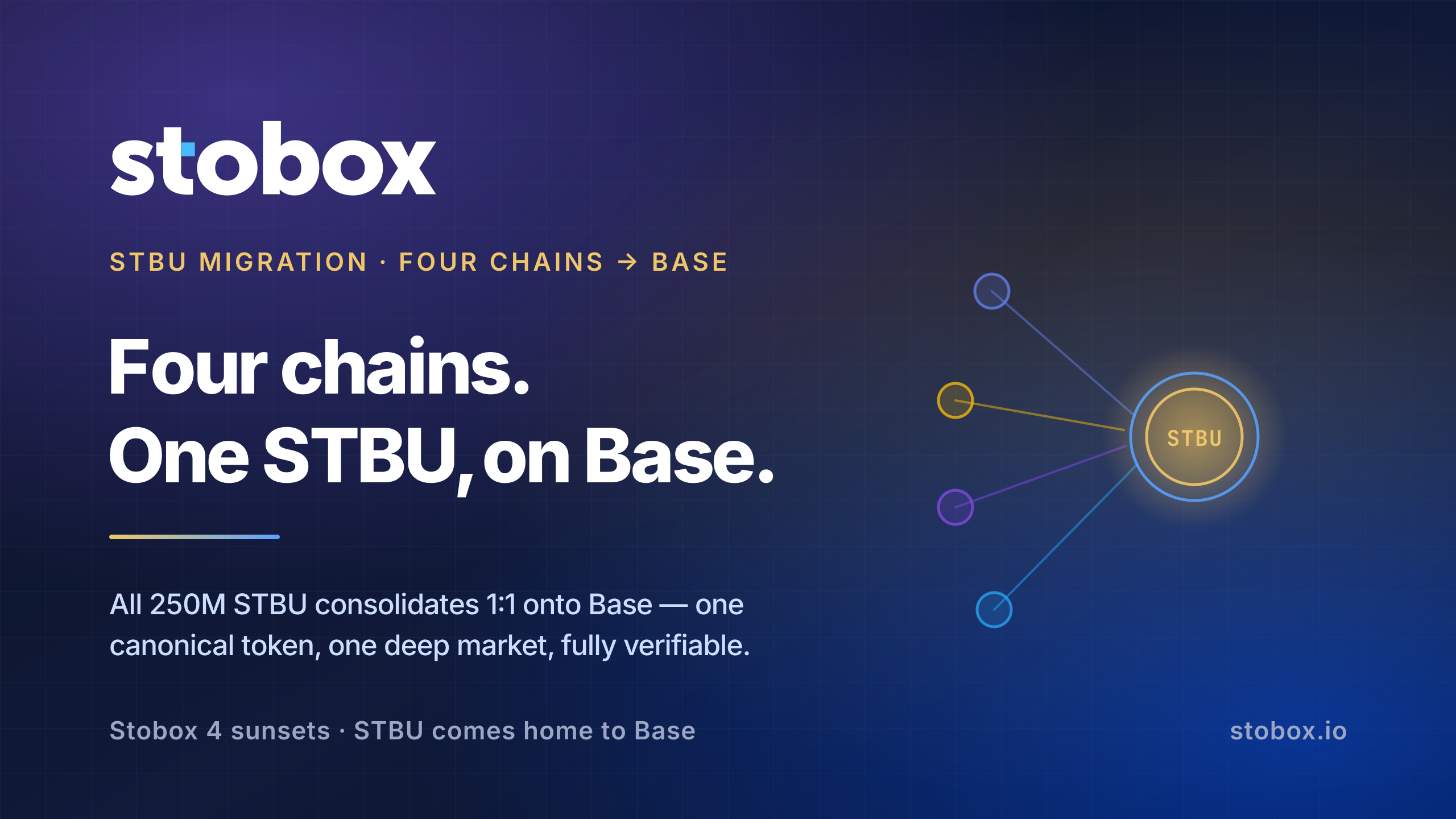

- From Stobox: STBU is consolidating 1:1 onto Base as Stobox Compass launches, making Base the settlement home for Stobox’s own stack.

1. Ondo launches the first US custodial tokenized securities — and they actually carry shareholder rights

What happened. On July 1–2, Ondo Finance went live with tokenized versions of BlackRock’s iShares Core S&P 500 ETF (IVV) and Micron (MU) stock on Ethereum. This is the first production deployment of the “custodial model” that the SEC’s staff described in its January 2026 tokenized-securities statement: the underlying shares stay in traditional US custody, a registered transfer agent mints tokens 1:1 against them, and Broadridge integrates proxy voting and shareholder disclosures so token holders receive the same governance rights as a brokerage account holder. See the Broadridge press release and CoinDesk’s coverage.

Why it matters. Most “tokenized stock” products to date have been synthetic wrappers or offshore instruments that strip out voting and shareholder standing. This is the first time a US-compliant structure has delivered a tokenized equity that behaves like the real security — including the boring, essential parts like proxy voting and disclosures. That is the difference between a novelty and an instrument an institution can actually hold.

Business impact. For issuers, the custodial model is now a proven template rather than a whitepaper. If you are an asset owner or fund considering tokenized equity exposure, the questions to ask a vendor just changed: not “can you mint a token,” but “who is the registered transfer agent, how are shareholder rights delivered, and where does custody sit.” For investors, tokenized equities with genuine governance rights become a defensible position rather than a compliance liability.

Stobox Perspective. This is the pattern we have argued for since 2018: tokenization succeeds when the compliance and rights layer is treated as the product, not an afterthought bolted onto a smart contract. The token is the easy part. The transfer-agent relationship, the governance integration, and the custody chain are where projects live or die. Expect fast-follow copies of this exact structure — and expect the winners to be the ones who already have the regulatory relationships, not the ones racing to write more Solidity.

Related trend. This connects directly to the DTCC pilot (item 8) and the SEC’s pending rulemaking (item 9). A production custodial model, a clearinghouse building tokenized settlement, and formal rules on the agenda are three parts of the same story: the US is assembling an end-to-end compliant path for tokenized securities.

Key takeaways.

- First US-compliant tokenized equities with full shareholder rights are now live.

- The transfer agent plus governance integration — not the token — is the moat.

- This is a template competitors will replicate within quarters.

2. Securitize lists on the NYSE as a public company

What happened. Securitize — one of the largest RWA tokenization firms, with several billion in assets under administration across mandates tied to BlackRock, VanEck and others — completed a business combination with Cantor Equity Partners II and began trading on the New York Stock Exchange around July 2 under the ticker SECZ. The deal raised roughly $400M in gross proceeds, including an oversubscribed $225M PIPE. The closing and listing are documented in the company’s combination announcement and SEC filings.

Why it matters. A pure-play tokenization infrastructure company is now publicly listed on the most established exchange in the world. That is a legitimacy and liquidity event for the entire category — it gives public-market investors a direct way to underwrite the tokenization thesis, and it gives every other infrastructure firm a valuation reference point.

Business impact. Public status raises the disclosure and governance bar for the whole sector, which is good for enterprise buyers who need vendors that will still exist in five years. For asset owners evaluating tokenization partners, the balance-sheet strength and reporting discipline of a listed company become part of the diligence conversation.

Stobox Perspective. The market is beginning to price the infrastructure layer, not the speculation layer — and that is the correct place for capital to concentrate. Tokenization value does not accrue to another token that goes up; it accrues to the firms that make compliant issuance, transfer and reporting boring and repeatable. A listing validates that infrastructure-first framing. It also raises the competitive bar: differentiation now comes from breadth of licensing and depth of compliance tooling, not from a press release.

Related trend. Read alongside the Open USD consortium (item 7) and JPMorgan’s growing fund (item 5): capital and institutions are consolidating around the plumbing of tokenized markets, not the assets alone.

Key takeaways.

- The leading tokenizer is now NYSE-listed (SECZ), roughly $400M raised.

- Public markets can now underwrite tokenization infrastructure directly.

- Expect a valuation benchmark that reshapes the competitive field.

3. Ripple wins full MiCA authorization across the EEA

What happened. On July 6, Luxembourg’s financial regulator (the CSSF) upgraded Ripple’s preliminary crypto-asset service provider license to a full MiCA authorization. That lets Ripple offer regulated crypto payment services, its RLUSD stablecoin, and XRP-based rails across all 30 European Economic Area countries. It builds on an earlier EMI license, giving Ripple a rare dual-license position in Europe. Details are in Ripple’s announcement and CoinDesk.

Why it matters. MiCA’s promise is passporting: authorize once, operate across the bloc. Ripple is now one of the first major digital-asset firms to hold that passport in full. For any business planning tokenized-asset or stablecoin distribution into Europe, this is a live demonstration that the passport model works — and a signal of who your regulated counterparties will be.

Business impact. If your tokenization roadmap touches European investors, the compliant path now runs through a MiCA-authorized entity — either your own or a partner’s. That is a build-versus-partner decision that just got more concrete. Firms without an EU licensing strategy should treat this as a prompt to form one.

Stobox Perspective. Licensing is the real product in tokenized finance, and it is increasingly a moat you cannot fake. Stobox has spent years assembling regulated footing — an EU VASP registration and a Qatar Financial Centre license — precisely because distribution to real investors requires it. A marquee MiCA authorization confirms the direction of travel: the firms that win European tokenization will be the licensed ones, and the license is getting harder to obtain, not easier.

Related trend. Pair this with the end of MiCA’s transitional period (item 4). One firm getting authorized and 900 firms failing to are two sides of the same regulatory hardening.

Key takeaways.

- Ripple holds a full MiCA passport across 30 EEA countries.

- The EU passport model is now demonstrably working for a major player.

- European tokenization distribution runs through licensed entities from here.

4. MiCA’s transitional period ends — the EU is now a licensed-only crypto market

What happened. On July 1, MiCA’s 18-month transitional window closed with no extension. Authorization is now the sole gateway to EU crypto markets. In a June statement, ESMA instructed unauthorized providers to wind down and said late applications would face heightened scrutiny. By various counts the field shrank from roughly 1,200 registered firms to somewhere around 283 fully licensed ones. The primary source is ESMA’s public statement (exact licensed-firm counts vary by source and should be treated as approximate).

Why it matters. Europe just set a hard regulatory floor under tokenized-asset issuance and crypto services. The grace period where firms could operate on legacy national registrations is over. This thins the field to licensed operators and raises the credibility of anyone still standing.

Business impact. For asset owners and issuers, counterparty risk in Europe just dropped for licensed firms and spiked for unlicensed ones. Check that every European partner in your tokenization stack — issuance, custody, distribution — holds MiCA authorization. For tokenization startups, “we will get licensed later” is no longer a viable European strategy.

Stobox Perspective. This is the regulatory maturation we have expected: markets that professionalize by forcing out the unlicensed middle. It is not bad news for tokenization — it is the precondition for institutional capital to participate. Institutions cannot transact with counterparties that might be shut down next quarter. A licensed-only market is a more investable market, even if it is a smaller one this month.

Related trend. Connects to the SEC’s parallel path in the US (item 9). Two of the world’s largest markets are converging on the same message: tokenized assets are welcome inside the regulatory perimeter, and only inside it.

Key takeaways.

- The EU crypto market is now licensed-only, with no transitional cover.

- The field consolidated sharply toward authorized firms.

- Audit every European counterparty for MiCA authorization now.

5. JPMorgan’s tokenized money-market fund roughly doubles to about $693M

What happened. As of July 8, JPMorgan’s on-chain money-market fund reached about $693M in assets — roughly double its end-of-May level near $347M. The growth is driven by stablecoin issuers parking Treasury reserves on-chain to earn yield, because the GENIUS Act bars them from paying interest to stablecoin holders directly. The fund holds only Treasuries and Treasury-backed overnight repos, with a $1M minimum, per American Banker.

Why it matters. This is a clean, measurable example of regulation creating structural demand for tokenized products. The GENIUS Act’s design — stablecoins cannot pay yield — pushes issuer reserves into yield-bearing tokenized Treasury funds. The plumbing is doing exactly what the incentives dictate.

Business impact. If you issue or hold stablecoins, tokenized Treasury funds are becoming the default home for reserves that need to earn. If you run a treasury function, on-chain money-market instruments are moving from experiment to a real allocation option with a bank name attached.

Stobox Perspective. Watch the mechanism, not the headline number. The interesting part is that a rule change (no yield on stablecoins) mechanically routes billions into tokenized funds. This is how tokenized markets will actually scale — not through retail enthusiasm, but through regulation and treasury math making the tokenized version the rational choice. Tokenized cash-management is quietly becoming default infrastructure.

Related trend. Directly linked to the stablecoin restructuring in item 7 and the broader tokenized-Treasury total in our market table. Stablecoins and tokenized Treasuries are now a coupled system.

Key takeaways.

- JPMorgan’s tokenized MMF roughly doubled to about $693M by July 8.

- GENIUS Act mechanics are channeling stablecoin reserves into tokenized Treasuries.

- Regulation, not hype, is the demand driver worth tracking.

6. Figure’s tokenized HELOC token passes $20B — bigger than all tokenized Treasuries combined

What happened. According to CoinDesk analysis published July 11, Figure Technologies’ tokenized home-equity line-of-credit (HELOC) instrument reached about $20.1B as of July 7, up roughly $730M in three weeks. The HELOCs are recorded, financed and traded on the Provenance blockchain. That figure is larger than the entire tokenized US Treasury segment (about $15.16B) and many times the tokenized-stock market. See CoinDesk’s “3 surprising tokenization stats.” This figure comes from a single primary outlet and is best read as directional rather than a line item you can pull from a public dashboard.

Why it matters. The largest tokenized asset in the world is not a fund or a stablecoin — it is private consumer credit used as securitization plumbing. It shows where real on-chain volume actually lives: in the unglamorous back-end of lending, where tokenization cuts settlement and financing friction.

Business impact. For private-credit originators and structured-finance teams, tokenization is already a working cost-reduction tool, not a future concept. For investors, the lesson is to look past the categories that get headlines (stocks, Treasuries) toward where tokenization is quietly compounding: credit and securitization.

Stobox Perspective. This is the most under-discussed fact in tokenization right now. The market fixates on tokenized equities and Treasuries because they are legible, but the volume leader is credit infrastructure most people never see. Tokenization wins first where it removes operational friction from something businesses already do — not where it invents a new consumer behavior. Expect more balance-sheet and securitization use cases to scale before retail ones do.

Related trend. Ties to New York Life and Centrifuge (item 10) and the private-credit theme in our market trends. Institutional credit is the quiet engine of RWA growth.

Key takeaways.

- Figure’s tokenized HELOC reached roughly $20.1B — the single largest tokenized asset.

- Private credit, not Treasuries or stocks, leads real on-chain volume.

- Tokenization scales first as back-end plumbing, not a retail product.

7. An Open USD stablecoin consortium forms — and Circle drops sharply

What happened. As the week opened, an independent operator unveiled “Open USD” (OUSD), a stablecoin that returns reserve income to participating businesses rather than keeping it, backed by a consortium reported to include Coinbase, Visa, Mastercard, Stripe and BlackRock. The model shares reserve revenue with merchants and launches natively on Solana, with more chains planned. Circle shares fell sharply — around 16% — on the news. See The Block and CoinDesk. (Announced June 30, this is the story shaping the current week.)

Why it matters. Stablecoins are the settlement layer under most RWA activity. A merchant-owned, revenue-sharing model directly attacks the economics that made Tether and Circle so profitable — keeping the reserve yield. If reserve income flows to the businesses using the stablecoin, the competitive basis of the entire stablecoin market shifts.

Business impact. For any company settling tokenized assets in stablecoins, the menu of rails just expanded, and the economics may improve. For issuers, stablecoin choice becomes a strategic decision about who captures the float, not just a technical one.

Stobox Perspective. Follow the reserve yield — it is the real prize in stablecoins, and control of it is now contested. The settlement layer under tokenization is being restructured around who keeps the float. That matters more to tokenized-asset issuers than most token launches, because it changes the cost and control of settlement itself. Watch whether regulated distribution or revenue-sharing wins; both are now in play.

Related trend. Directly coupled with JPMorgan’s tokenized MMF (item 5): as stablecoins compete on reserve economics, the yield those reserves seek lands in tokenized Treasury funds.

Key takeaways.

- A merchant-owned, revenue-sharing stablecoin (Open USD) entered the field.

- The attack is on reserve economics — the core of stablecoin profitability.

- Settlement-layer competition matters directly to RWA issuers.

8. DTCC moves its tokenized-securities platform toward go-live

What happened. The DTCC — the clearinghouse behind the vast majority of US securities processing — has a tokenized-securities platform built on its ComposerX infrastructure, with a pilot targeted to open in July and a full service launch targeted for October 2026. More than 50 firms are named as participants, including BlackRock, Goldman Sachs, JPMorgan, Circle, Ondo and Ripple. The program was announced in early May via CoinDesk. Note: the announcement is solid, but we did not find a July primary release confirming executed pilot trades — treat the pilot as opening, not proven.

Why it matters. If tokenized securities are going to clear and settle at institutional scale in the US, they will likely do it through the DTCC or something that looks like it. The core plumbing of US capital markets preparing to handle tokenized instruments is the single biggest structural signal that tokenization is moving from the edge to the center.

Business impact. For issuers and funds, DTCC involvement means tokenized securities may soon settle inside the same trusted rails as conventional ones — reducing the “is this real infrastructure” objection from institutional counterparties. Track the October milestone as a gating event for institutional tokenized issuance.

Stobox Perspective. When the clearinghouse moves, the market follows. This is the difference between tokenization as a parallel experiment and tokenization as an upgrade to existing market structure. The firms positioned to benefit are those already integrated with regulated settlement and transfer-agent workflows — because that is the surface DTCC’s model will connect to.

Related trend. The natural counterpart to Ondo’s custodial launch (item 1) and the SEC’s rulemaking (item 9): production issuance, institutional settlement, and formal rules advancing together.

Key takeaways.

- DTCC’s tokenized-securities pilot is targeted to open in July, launch in October.

- 50-plus major firms are participating, signaling broad institutional buy-in.

- October is the milestone to watch; pilot execution is not yet independently confirmed.

9. SEC tokenized-securities rulemaking sits on the agenda for July

What happened. Several SEC proposals relevant to tokenized securities are at the proposed-rule stage with July 2026 target dates, including a digital-asset offerings rule and broker-dealer and market-structure amendments touching custody and recordkeeping. These build on the SEC staff’s January 28, 2026 statement establishing a taxonomy for tokenized securities. See the SEC’s tokenized-securities statement. Important: these are target dates on the regulatory agenda. We found no confirmation that any of these proposals were actually published during this window — do not read this as “rules issued.”

Why it matters. Formal SEC rules would give US tokenized securities a defined registration and custody framework — the biggest pending regulatory catalyst for the American market. The January taxonomy already gave the market a shared vocabulary (that is what enabled Ondo’s custodial launch). Actual proposed rules would be the next step from vocabulary to framework.

Business impact. For US issuers, this is a “prepare, do not wait” signal. The direction is clear even if the timing is not. Structure tokenization projects to fit the custodial model the SEC has already described, so you are aligned when rules land rather than retrofitting later.

Stobox Perspective. Regulatory clarity is the unlock, and it usually arrives as taxonomy first, rules second, adoption third. The US is visibly walking that path. The mistake would be to treat “no final rule yet” as “no signal.” The signal is loud: build compliant, build for the custodial model, and be ready. Firms that wait for perfect certainty will be a year behind the ones building against the published direction.

Related trend. Mirrors the EU’s MiCA hardening (items 3 and 4). The two largest capital markets are both formalizing tokenization inside their regulatory perimeters.

Key takeaways.

- SEC tokenized-securities proposals are on the agenda with July target dates.

- No rules were confirmed issued this week — treat as expected, not done.

- Build to the SEC’s already-published custodial model now.

10. New York Life and Centrifuge bring an $800B insurer into tokenized credit

What happened. In late June, New York Life — an insurer with roughly $800B in assets under management — made its tokenization debut with an on-chain high-yield bond fund built with Centrifuge, as reported by CoinDesk. It is one of the largest traditional insurers to put a fund on-chain, and it lands squarely in the private-credit category that is quietly leading RWA growth.

Why it matters. Insurers are among the most conservative and heavily regulated allocators in finance. When an $800B insurer tokenizes a fund, it tells every other large allocator that the operational and compliance questions have credible answers. It also reinforces that credit — not equities — is where large institutional tokenization is happening first.

Business impact. For fund managers, tokenized fund structures now have blue-chip precedent to point to in fundraising and diligence conversations. For investors, the entry of insurers signals deepening institutional liquidity in tokenized credit specifically.

Stobox Perspective. Conservative capital moves last and moves in size. An insurer’s debut is a lagging indicator that the infrastructure is finally trusted — and a leading indicator of the volume that follows once it is. The category to watch remains tokenized credit, where the combination of yield, securitization efficiency and institutional comfort is compounding fastest.

Related trend. Completes the private-credit theme running through Figure’s HELOC token (item 6) and our market trends below. Credit is the connective tissue of this week’s story.

Key takeaways.

- An $800B insurer entered tokenized credit via Centrifuge.

- Insurer participation is a strong trust signal for large allocators.

- Tokenized credit remains the leading institutional category.

Market Trends This Week

Step back from the individual stories and a coherent picture forms.

Institutional adoption crossed from pilots to production. Ondo shipped compliant tokenized equities, DTCC advanced institutional settlement, and an $800B insurer went on-chain — all in one week. The actors are no longer crypto-native startups; they are clearinghouses, transfer agents, banks and insurers.

Regulation is the primary driver, in both directions. The EU hardened into a licensed-only market while the US advanced a taxonomy toward rules. Regulation is not slowing tokenization; it is shaping who gets to do it and channeling demand (GENIUS Act reserves into tokenized Treasuries being the cleanest example).

Infrastructure and settlement are where value concentrates. Securitize’s NYSE listing prices the infrastructure layer. DTCC’s platform and Ondo’s transfer-agent model show that the winners build plumbing, not tokens. Interoperability efforts like Swift and Chainlink’s ongoing settlement trials point the same way, though those remain in testing.

Private credit leads real volume. Figure’s roughly $20B HELOC token dwarfs tokenized Treasuries and stocks. Credit and securitization — not retail-facing assets — are where tokenization is compounding.

Stablecoins are being restructured around reserve economics. The Open USD consortium’s revenue-sharing model attacks the float that made incumbents profitable, and that reshapes the settlement layer beneath every tokenized asset.

Here is the market by the numbers. Note that totals diverge because sources measure different things — liquid and freely transferable on-chain value is not the same as “represented” value or all-products-including-permissioned.

| Metric | Value | As of | Note |

|---|---|---|---|

| Tokenized RWA — liquid on-chain | ~$33.5B, ~959K holders | Jul 8, 2026 | via outlets citing rwa.xyz |

| Tokenized RWA — all products | ~$60B across ~7,000 products | Jul 2, 2026 | much of it dormant |

| Tokenized US Treasuries | ~$15.16B | Jul 7, 2026 | CoinDesk analysis |

| BlackRock BUIDL | ~$2.4–2.5B | Jul 2026 | largest tokenized Treasury fund |

| Figure HELOC token | ~$20.1B | Jul 7, 2026 | largest single tokenized asset |

| Stablecoin market cap | ~$290–308B | Jul 2026 | USDT ~$184B |

We are deliberately not printing a single private-credit total this week — the figures we found conflated private credit with the broader on-chain total, and we would rather omit a number than publish one we cannot stand behind.

What This Means for Asset Owners

Should you tokenize now, or wait? For most asset owners, the honest answer this week shifted toward “start preparing now.” The custodial model is proven, the EU and US regulatory directions are legible, and institutional counterparties (clearinghouses, insurers, banks) are participating. Waiting for total certainty means arriving a year behind peers who built against the published direction.

Where the opportunities are. The clearest openings are in credit and fund structures, where institutional comfort is highest and the operational case is strongest. Real estate, private equity and infrastructure follow the same playbook: the value is in compliant issuance and efficient administration, not in the novelty of a token.

The common, expensive mistakes. First, treating tokenization as a technology project rather than a compliance and structuring project — the token is the last 10% of the work. Second, choosing counterparties without verifying licensing (now a hard requirement in the EU). Third, building a bespoke structure when a proven model — like the custodial approach the SEC described — already exists. Learn the difference between a security token and a utility token before you design anything, and pressure-test readiness before you commit capital.

If you want a structured read on whether your specific asset is ready, our tokenization readiness tooling is built for exactly that question.

What This Means for Investors

Where capital is flowing. Toward infrastructure and toward credit. Securitize’s listing lets public-market investors underwrite the picks-and-shovels layer directly. Figure’s HELOC token and New York Life’s fund show that private credit is where on-chain volume actually accumulates.

Which sectors are growing. Tokenized Treasuries continue their steady climb as stablecoin reserves seek yield. Tokenized credit is growing fastest in absolute terms. Tokenized equities are now credible but still small — the interesting development there is governance rights, not volume.

Which infrastructure is winning. The firms with regulatory footing and settlement integration: transfer agents, clearinghouses, licensed service providers. The lesson from this week is that infrastructure with compliance built in — not the flashiest protocol — captures the durable value. For a deeper framing, see our note on tokenization for investors.

Stobox Insights

We are not going to sell you anything in this section. Here is what we actually observe.

The pattern. Every major development this week rewarded the same thing: compliance and settlement infrastructure built before the hype, not after. Ondo’s transfer-agent model, Ripple’s license, DTCC’s clearing rails, the EU’s licensed-only market — the winners already had the regulatory and operational groundwork. Tokenization is maturing into a business where the unglamorous layer is the whole game.

What happens next. Expect fast replication of the US custodial model, an October gating event around DTCC’s launch, and continued consolidation of value into licensed infrastructure. Expect the stablecoin reserve-economics fight to intensify, because whoever controls the float controls the settlement layer. And expect credit to keep leading volume while equities lead headlines.

What companies should prepare for. Licensing is becoming non-negotiable, not a later step. The custodial model is becoming the reference architecture for tokenized securities. And interoperability — the ability to move tokenized assets between institutions and chains — is moving from nice-to-have toward mandatory. Standards like ERC-3643 for permissioned tokens, and newer universal RWA interfaces, are becoming the technical baseline for institutional acceptance.

Where the opportunities are. For operators: build compliant, build to the emerging reference models, and secure regulatory footing early. For asset owners: the assets with clear cash flows and clean legal structures — credit, funds, income-producing real estate — are ready first. The window to be early is still open, but it is closing at the pace of regulation, not the pace of technology.

From Stobox: STBU consolidates onto Base as Compass launches

We hold ourselves to the same “show your work” standard we apply to everyone else, so here is what changed on our side this week. Stobox is consolidating its STBU utility token onto a single contract on Base, migrating 1:1 from Ethereum, BNB Chain, Polygon and Arbitrum — every token on the old chains mints the same amount on Base, to the same address. It lands alongside the launch of Stobox Compass, the guided workflow that takes a tokenization project from readiness assessment to issuance, with STBU as the working asset that unlocks higher tiers.

The reason it belongs in this digest: it is the same pattern the week’s institutional stories describe, applied to our own infrastructure. As Ondo issues on Ethereum, JPMorgan grows a tokenized fund, and the DTCC builds tokenized settlement, the direction is toward consolidating activity onto credible, liquid public chains rather than fragmenting across many. Building STBU on the Base and broader Coinbase stack is our version of that same bet: put the working asset where the compliance tooling, wallets and liquidity are converging. Details are on the STBU page, and the full rationale is in our note on the new Stobox as one system.

This is the only place in the digest where we cover ourselves — the ten developments above were selected on their importance to the industry, not to us.

Explore tokenization with Stobox

Thinking about tokenizing an asset — real estate, a fund, private equity, infrastructure, commodities, carbon credits, intellectual property, or corporate equity? Stobox has built compliance-first tokenization infrastructure since 2018, and we help businesses design, issue and manage compliant tokenized assets from strategy through launch. Start with our tokenization overview, or subscribe to this digest to get the weekly briefing in your inbox every Tuesday.

Frequently Asked Questions

What happened in tokenization this week? The biggest developments were Ondo launching the first US custodial tokenized securities (tokenized BlackRock IVV and Micron shares with full shareholder rights), Securitize listing on the NYSE under ticker SECZ, Ripple winning full MiCA authorization across the EEA, the end of MiCA’s transitional period on July 1, and JPMorgan’s tokenized money-market fund roughly doubling to about $693M.

Is RWA tokenization still growing? Yes. Liquid, freely transferable tokenized real-world assets sit near $33.5B on-chain as of early July 2026, held by roughly 959,000 holders, and closer to $60B if you include permissioned and dormant products. Growth is led by tokenized credit and tokenized Treasuries.

How large is the tokenization market? Estimates vary by definition. Liquid on-chain value is around $33.5B; total tokenized products including permissioned and dormant ones are around $60B; “represented” asset value (committed but not freely transferable) is cited in the hundreds of billions. Always check which definition a figure uses.

Who is leading RWA tokenization? By infrastructure, firms like Securitize (now NYSE-listed), Ondo and Centrifuge. By single-asset size, Figure’s tokenized HELOC token (about $20.1B). By tokenized Treasuries, BlackRock’s BUIDL (about $2.4–2.5B). Institutions like JPMorgan, New York Life and the DTCC are now active participants.

What is tokenized private credit? Tokenized private credit is private lending — such as home-equity lines, corporate loans or high-yield bond funds — recorded and traded on a blockchain. It is currently the largest category of tokenized real-world assets by on-chain volume, because tokenization reduces settlement and financing friction in securitization.

What are tokenized treasuries? Tokenized Treasuries are on-chain funds or instruments backed by US government debt, giving holders yield-bearing exposure to Treasuries in token form. The segment sits around $15.16B, with BlackRock’s BUIDL the largest single fund. Stablecoin issuers increasingly use them to earn yield on reserves.

Why are banks and institutions adopting tokenization? Because it reduces settlement time, cuts operational cost, and — under rules like the GENIUS Act — creates structural demand (for example, stablecoin reserves seeking on-chain yield). This week JPMorgan, the DTCC and insurer New York Life all advanced tokenization initiatives.

What is ERC-3643? ERC-3643 is a token standard for permissioned (compliant) security tokens that enforces identity and transfer-eligibility rules on-chain, so only approved investors can hold or trade a token. It is a common technical baseline for regulated tokenized securities. See our glossary for related terms.

What is the custodial model for tokenized securities? In the custodial model, the underlying security stays in traditional regulated custody, a registered transfer agent mints blockchain tokens 1:1 against it, and shareholder rights (like proxy voting) are delivered to token holders. Ondo’s July launch with BlackRock IVV and Micron shares is the first US production example.

What did the end of MiCA’s transitional period mean? As of July 1, 2026, firms can only offer crypto-asset services in the EU with full MiCA authorization — the grace period for operating on legacy national registrations ended. The market consolidated toward licensed firms, and unlicensed providers were told to wind down.

Should I tokenize my asset now or wait? For most asset owners with clean legal structures and clear cash flows — credit, funds, income-producing real estate — the case for preparing now strengthened this week, given proven compliant models and clear regulatory direction. The common mistake is treating tokenization as a technology project rather than a compliance and structuring one.

How do I tokenize real estate or a fund? The process centers on legal structuring, compliance (investor eligibility, jurisdiction, licensing), choosing a token standard and issuance platform, and ongoing administration. The token itself is the last step. Stobox provides tokenization infrastructure that covers strategy through launch and ongoing management.

Where can I follow the Stobox Weekly RWA & Tokenization Digest? This digest publishes every Tuesday. You can subscribe to receive it by email, and read past editions on the Stobox blog.