Stablecoins are the most successful product cryptocurrency has ever shipped. As of mid-July 2026, roughly $303 billion in stablecoins circulate on public blockchains, and they settle more value each year than most national payment systems. They are the cash leg of crypto trading, the settlement rail for tokenized real-world assets, a dollar account for people in weak-currency economies, and — since the GENIUS Act became law — the first crypto instrument with a dedicated US federal regulatory regime.

This week is also a milestone: July 18, 2026 is the statutory deadline for US federal agencies to publish the final rules implementing the GENIUS Act, one year to the day after it was signed. The era of stablecoins as a regulatory gray zone is ending in real time.

This guide covers the full picture: what stablecoins are, the three fundamental designs and the trilemma that connects them, the history of failures that shaped today’s rules, the state of regulation in the US, EU, UK and Asia as of July 2026, and a ranked look at the leading stablecoins today. It is written for business operators, asset owners and investors who need to understand stablecoins as financial infrastructure — not as speculation.

What is a stablecoin?

A stablecoin is a blockchain-based token designed to hold a stable value against a reference asset — almost always the US dollar, increasingly the euro, and occasionally gold or other currencies. One token targets a value of exactly one unit of the reference asset: 1 USDT ≈ $1, 1 EURC ≈ €1.

The point of a stablecoin is to combine two things that never previously coexisted:

- The stability of fiat money. Prices, invoices, salaries and settlement obligations are denominated in dollars or euros. An asset that swings 10% in a day cannot be a unit of account or a working medium of exchange.

- The properties of a blockchain asset. Stablecoins settle in seconds to minutes, move 24/7/365 across borders, cost cents to transfer, are programmable (they can be escrowed, streamed, or released against conditions in a smart contract), and interoperate natively with tokenized assets.

That combination is why stablecoins found real product-market fit while most crypto assets remained speculative. In practice they are used for:

- Trading and market liquidity — the quote currency for most crypto pairs and the parking asset between positions.

- Cross-border payments and B2B settlement — treasury transfers that clear in minutes instead of the multi-day correspondent-banking chain.

- Dollar access in weak-currency economies — a de facto offshore dollar account for individuals and businesses facing inflation or capital controls.

- On-chain settlement for tokenized assets — when a tokenized security trades, the cash side of the trade needs to be on-chain too. Stablecoins are that cash side, enabling true delivery-versus-payment where the asset and the money move in one atomic transaction.

The last use case is the one we care most about at Stobox: tokenized real-world assets only deliver their promised settlement efficiency if the money itself is on-chain. Stablecoins are the money.

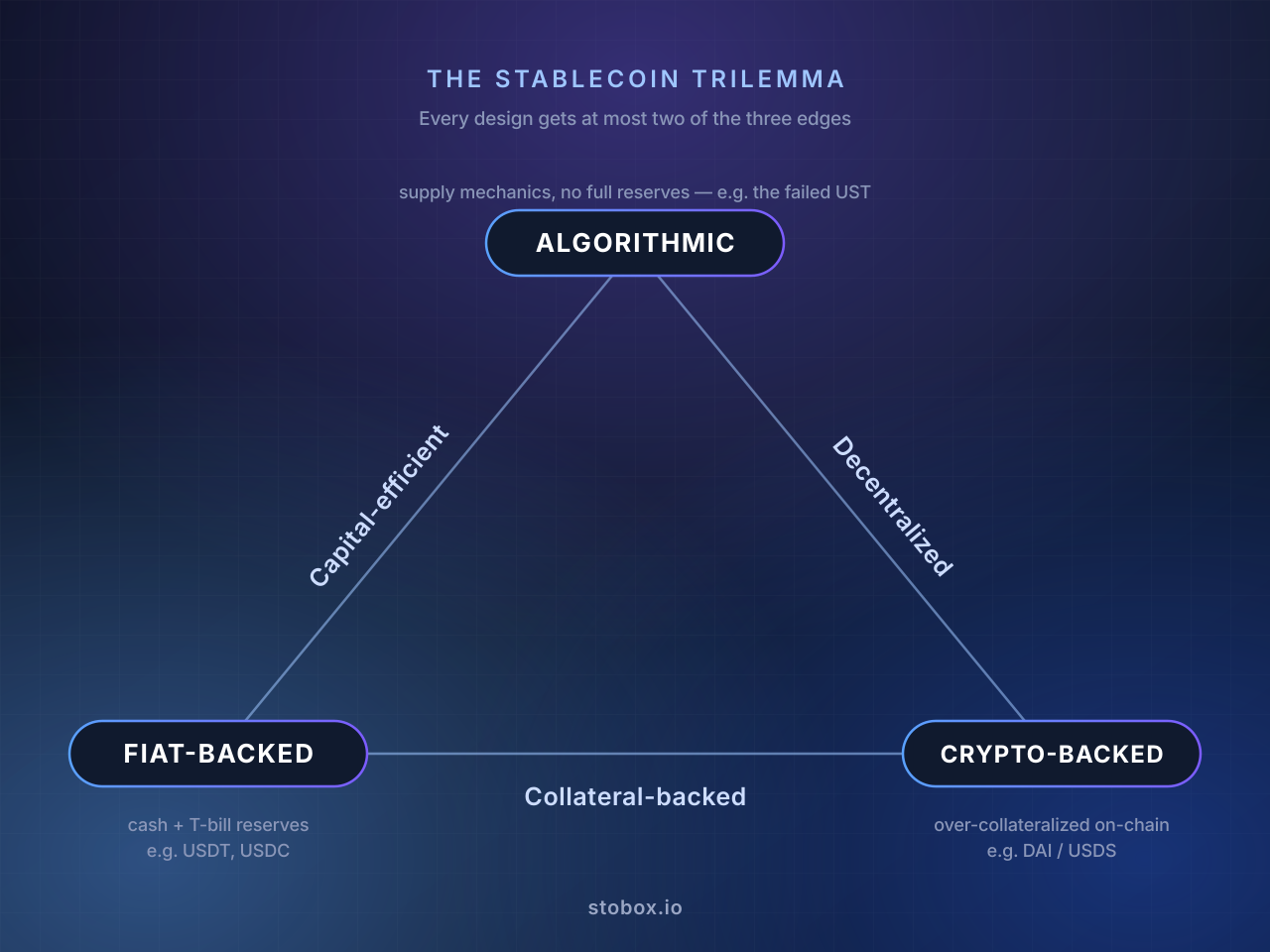

The stablecoin trilemma: one triangle that explains every design

Every stablecoin ever launched is an answer to one question: what makes the token worth $1? There are only three fundamental answers, and they form the triangle above — the same trilemma diagram we use when explaining stablecoin design (you may have seen the Russian-language version in our video materials; here is exactly what it shows).

The three corners are the three collateral models:

- Fiat-backed stablecoins (bottom left — think Tether’s USDT, Circle’s USDC). Real dollars and US Treasury bills sit in bank and custody accounts; the issuer mints one token per dollar received and redeems one dollar per token returned.

- Crypto-backed stablecoins (bottom right — think DAI, now largely migrated to Sky’s USDS). The collateral is other crypto assets, locked in smart contracts in excess of the stablecoin’s value.

- Algorithmic stablecoins (top — the model behind Basis and Terra’s UST). No collateral, or only partial collateral. A protocol algorithmically expands and contracts supply, or offers arbitrage against a sister token, to hold the peg.

The edges of the triangle are the properties each pair of designs shares — and, by implication, the property each corner gives up:

- The bottom edge — “collateral-backed.” Fiat-backed and crypto-backed designs share it: every token is backed by something real that can be liquidated. Algorithmic designs sit at the opposite vertex because they gave this up — that is precisely what made them fragile.

- The left edge — “capital-efficient.” Fiat-backed and algorithmic designs share it: creating $1 of stablecoin requires $1 of reserves (fiat-backed) or, in theory, nothing at all (algorithmic). Crypto-backed designs give this up — because crypto collateral is volatile, you must lock up $1.50–$2.00 of it to safely issue $1 of stablecoin.

- The right edge — “decentralized.” Crypto-backed and algorithmic designs share it: they live entirely on-chain, with no bank account to freeze and no single company that can be shut down. Fiat-backed designs give this up — they depend on banks, custodians and a central issuer that can freeze addresses and must obey court orders.

The trilemma’s uncomfortable conclusion: you can have at most two of stability-through-collateral, capital efficiency, and decentralization. Pick collateral and capital efficiency, and you get a centralized instrument (USDT, USDC). Pick collateral and decentralization, and you get an over-collateralized, capital-hungry instrument (DAI/USDS). Pick capital efficiency and decentralization — and you get an algorithmic design that history suggests eventually breaks.

The market has voted. Fiat-backed designs are roughly 95% of all stablecoin value today. Regulators have voted the same way: every major regime enacted since 2023 — the GENIUS Act, MiCA, Hong Kong’s Stablecoins Ordinance, the UK’s forthcoming rules — effectively mandates the fiat-backed corner of the triangle and, in several jurisdictions, bans the algorithmic corner outright. Understanding the trilemma is therefore not academic: it explains both the market structure and the shape of the law.

Let’s take each corner in turn.

Fiat-backed stablecoins: the corner that won

How they work. A central issuer (Tether, Circle, Paxos, PayPal) receives dollars from customers, holds them in reserve, and mints an equivalent number of tokens. Redemption reverses the flow: return tokens to the issuer, receive dollars. The peg is maintained by arbitrage — if the token trades at $0.99, arbitrageurs buy it and redeem at $1.00; if it trades at $1.01, they mint at $1.00 and sell.

What the reserves actually are. The modern reserve model — now codified in the GENIUS Act — is cash, overnight repos and short-dated US Treasury bills, with monthly public disclosures. This makes major stablecoin issuers structurally similar to government money-market funds, and collectively a significant holder of US government debt: Tether alone holds a Treasury portfolio that would rank it among the larger sovereign holders of US debt.

Strengths. Simplicity, deep liquidity, the tightest pegs in the market, and — post-GENIUS — a clear legal status. Capital efficiency is perfect: $1 in, $1 out.

Weaknesses. Centralization is total. The issuer can freeze addresses (and routinely does, under sanctions and law-enforcement orders). Users carry issuer credit risk and, indirectly, banking risk — the March 2023 USDC depeg happened not because of anything on-chain, but because $3.3 billion of Circle’s reserves were briefly trapped in Silicon Valley Bank when it failed. USDC fell to roughly $0.87 before recovering when US authorities guaranteed SVB deposits. The lesson stuck: a fiat-backed stablecoin is only as strong as its reserve custody chain.

Who uses them. Essentially everyone. USDT dominates trading and emerging-market dollar demand; USDC dominates regulated institutional flows, DeFi blue chips and US-domiciled platforms.

Crypto-backed stablecoins: decentralization at a capital cost

How they work. Instead of dollars in a bank, the collateral is crypto — ETH, liquid staking tokens, tokenized T-bills — locked in an on-chain vault. Because that collateral is volatile, the system requires over-collateralization: to mint $100 of stablecoin you might lock $150–$200 of collateral. If the collateral’s value falls toward the debt, the position is automatically liquidated — the collateral is auctioned to buy back and burn the stablecoin, keeping every token backed.

The reference implementation is MakerDAO’s DAI, launched in 2017 and the longest-surviving decentralized stablecoin. In 2024–2025 Maker rebranded to Sky and introduced USDS as DAI’s successor; by April 2026 most exchanges had converted DAI balances to USDS, and the two together represent roughly $15 billion. It is worth noting that modern DAI/USDS is a hybrid: a meaningful share of its backing is real-world assets and USDC, which trades away some decentralization purity for stability and scale — the trilemma asserting itself again.

Strengths. No bank in the loop, no single company to subpoena, fully transparent collateral visible on-chain in real time, censorship resistance.

Weaknesses. Capital inefficiency (that locked excess collateral has a cost), liquidation cascades in fast crashes (Black Thursday, March 2020, forced emergency changes in Maker), oracle risk (the system is only as good as its price feeds), and governance risk. And regulators have not yet decided what these instruments are: the GENIUS Act’s framework simply does not contemplate an issuerless stablecoin, which leaves decentralized designs in a legal gray zone precisely as the compliant corner of the market gets formalized.

Algorithmic stablecoins: the corner that failed

How they were supposed to work. An algorithmic stablecoin holds its peg through supply mechanics rather than collateral. The best-known design — Terra’s UST — allowed anyone to burn $1 worth of the sister token (LUNA) to mint 1 UST, and burn 1 UST to mint $1 of LUNA. As long as LUNA had value and the market believed in the mechanism, arbitrage held the peg, and no dollar of reserves was needed. Perfect capital efficiency, full decentralization — the seductive third corner of the triangle.

How they actually failed. The mechanism is reflexive: the stablecoin’s backing is confidence in an asset whose value largely derives from demand for the stablecoin itself. In May 2022, large UST withdrawals cracked the peg; arbitrageurs burned UST and minted LUNA to capture the spread; LUNA supply hyperinflated from ~350 million to over 6.5 trillion tokens in days; its price collapsed toward zero, taking the “backing” with it. Roughly $18 billion of UST and about $40 billion of LUNA value evaporated inside a week — approximately $60 billion in total, the largest single value destruction event in crypto history. The collapse took down lenders and funds (Celsius, Three Arrows Capital) and, more consequentially, triggered the global regulatory response that produced today’s stablecoin laws.

The regulatory verdict. The GENIUS Act ordered a Treasury study of “endogenously collateralized” stablecoins rather than permitting them; MiCA’s rules on asset-referenced tokens effectively exclude them from the EU market; Hong Kong’s regime requires full backing by high-quality liquid assets. In every major jurisdiction, the algorithmic corner of the triangle is now either banned or regulated out of practical existence.

The nuance worth keeping. “Algorithmic” became a slur, but the underlying question — can you make a dollar with less than a dollar of dead capital behind it? — did not go away. It migrated into designs that are collateralized but capital-clever, which brings us to the hybrid frontier.

The hybrid frontier: synthetic dollars and yield-bearing tokens

Two newer categories sit deliberately between the triangle’s corners:

Synthetic dollars. Ethena’s USDe (roughly $4 billion as of spring 2026) holds crypto collateral but hedges it delta-neutral with short perpetual-futures positions — the collateral’s volatility is cancelled by the hedge, so full backing is achieved without over-collateralization. It also passes through the yield the hedge earns. It is not an algorithmic stablecoin — it is fully collateralized — but its stability depends on derivatives markets functioning and funding rates behaving, a different and still only partially tested risk profile. Ethena itself labels USDe a “synthetic dollar” rather than a stablecoin, which is the honest framing.

Yield-bearing and tokenized-Treasury tokens. Ondo’s USDY (~$1.3 billion) and similar instruments wrap short-term US Treasury exposure in a transferable token that accrues yield to the holder. These blur into tokenized money-market funds — BlackRock’s BUIDL is the institutional flagship — and they matter because of a regulatory fault line we’ll return to: the GENIUS Act prohibits regulated payment stablecoins from paying interest. Every basis point of Treasury yield earned on stablecoin reserves goes to the issuer, not the holder. That makes yield-bearing alternatives structurally attractive to treasurers and funds, and it is why the sharpest lobbying fight in Washington’s market-structure debate is precisely about stablecoin yield.

What history taught us: a short depeg record

Every design above has been stress-tested. The record is worth thirty seconds:

| Event | Date | Design lesson |

|---|---|---|

| Iron Finance (IRON/TITAN) collapse | June 2021 | Partial collateral + reflexive token = bank run; a dress rehearsal for Terra |

| TerraUSD (UST) collapse, ~$60B destroyed | May 2022 | Uncollateralized pegs die by reflexivity; triggered global stablecoin legislation |

| USDT brief depeg to ~$0.95 | May 2022 | Contagion pressure; recovered via redemptions — reserves held |

| USDC depeg to ~$0.87 (SVB failure) | March 2023 | Fiat-backed coins carry banking risk in the reserve chain |

| USDR (real-estate-backed) depeg | October 2023 | Illiquid collateral cannot back an instantly redeemable liability |

Three durable lessons: collateral quality and liquidity matter more than collateral quantity; redemption is the peg (any friction in converting token to dollar is where runs begin); and transparency is a stabilizer — the issuers that survived stress were the ones whose reserves the market could verify quickly.

Stablecoin regulation in 2026: the year the rules arrived

Between 2014 and 2023, stablecoins scaled from zero to a quarter-trillion dollars with essentially no dedicated regulation anywhere. Between 2023 and 2026, every major financial jurisdiction built a regime. Here is where each stands as of July 14, 2026.

The GENIUS Act: the US federal stablecoin law

The Guiding and Establishing National Innovation for U.S. Stablecoins Act — the GENIUS Act — was signed into law on July 18, 2025, the first US federal statute dedicated to a crypto asset class. Its core provisions:

- Only “permitted payment stablecoin issuers” may issue. Three routes: subsidiaries of insured depository institutions; federally qualified nonbank issuers supervised by the OCC; or state-qualified issuers (available while an issuer remains under $10 billion outstanding, in states whose regimes Treasury certifies as substantially similar to the federal one).

- 1:1 reserves in the safest assets only. US currency and deposits, short-dated Treasury bills, overnight repos backed by Treasuries, and government money-market funds. No corporate paper, no crypto, no duration games.

- Monthly public reserve disclosures, examined by a registered accounting firm, with CEO/CFO certifications carrying personal liability.

- No interest or yield may be paid to stablecoin holders by the issuer.

- Holder priority in insolvency — stablecoin holders rank first against reserve assets if an issuer fails.

- Full AML/sanctions obligations — issuers are Bank Secrecy Act financial institutions and must be able to freeze and burn tokens on lawful order.

- A phase-in with teeth. After a transition period, digital-asset platforms may only offer compliant payment stablecoins in the US market — the commercial pressure that forces offshore issuers to either qualify, partner, or lose US distribution.

Where implementation stands right now. This is the live story of July 2026. The Act’s effective date is the earlier of January 18, 2027, or 120 days after primary regulators finalize implementing rules — and the statute set July 18, 2026 as the deadline for those final rules, one year after enactment. Six agencies — the OCC, FDIC, NCUA, Treasury, FinCEN and OFAC — published proposed rules across late 2025 and early 2026 (the OCC’s framework for nonbank issuers, an FDIC regime for bank subsidiaries, a joint FinCEN/OFAC rule implementing AML and sanctions-compliance programs, and a Treasury proposal on certifying state regimes). All major comment periods closed by June 9, 2026, and the agencies have spent the weeks since reconciling six frameworks into final text. As we publish, the deadline is four days away. Once final rules land, the 120-day clock starts, meaning the GENIUS regime becomes fully operative around late 2026 to January 2027 — and every issuer that wants US distribution is already on the clock.

What it changes in practice. For businesses, GENIUS converts stablecoins from a counterparty-risk judgment call into a supervised instrument category: a compliant payment stablecoin will be, functionally, a bearer money-market share with full reserve transparency and a federal examiner behind it. For issuers, it entrenches the fiat-backed corner of the trilemma as the only US-legal design for payment stablecoins. And for banks, it opens the field: bank-issued stablecoins and deposit tokens (like JPMorgan’s JPMD on Base) now have a legal lane, which is why 2026 has become the year of bank-consortium stablecoin announcements.

The CLARITY Act: market structure, still in the Senate

The Digital Asset Market Clarity Act is the companion legislation — not a stablecoin law per se, but the bill that decides how the rest of the US crypto market is regulated, including how stablecoins are traded, custodied and integrated into exchanges. It divides oversight between the CFTC (digital commodities) and the SEC (securities and investment contracts), creates registration lanes for exchanges and brokers, and settles the decade-old “is it a security?” question with statutory definitions.

Status as of mid-July 2026: the bill passed the House on July 17, 2025 by 294–134 — the strongest bipartisan crypto vote in congressional history — and the Senate Banking Committee advanced its version 15–9 on May 14, 2026. A revised text was published June 1 and placed on the Senate legislative calendar. It now sits one step from a floor vote, with roughly five weeks of legislative runway before the summer recess and the midterm-election season effectively freeze major legislation.

Three fights are holding it: stablecoin yield (the Senate Banking draft prohibits platforms from paying interest on stablecoin balances — closing the loophole of “the issuer can’t pay yield, but your exchange can” — while allowing activity-based rewards; the crypto industry is fighting hard the other way); the DeFi developer shield versus law-enforcement objections; and political ethics provisions tied to the President’s own crypto interests. Whether CLARITY passes before the recess or slips into 2027 is genuinely uncertain — but for stablecoin users the practical takeaway is that the yield question, not the issuance question, is what remains unsettled in the US.

MiCA: Europe’s licensed-only market

The EU regulated first. MiCA (Markets in Crypto-Assets Regulation) applied its stablecoin provisions in June 2024: issuers of e-money tokens (fiat-referencing stablecoins) must be authorized as credit institutions or e-money institutions in the EU, hold fully backed segregated reserves (with minimum shares in bank deposits), publish a regulator-approved white paper, and honor redemption at par at all times. “Significant” tokens face enhanced supervision, and non-euro stablecoins face usage caps as a means of exchange within the EU — a deliberately dirigiste feature designed to protect euro monetary sovereignty.

Two consequences define the European market in 2026:

- USDT was effectively pushed out of regulated EU venues (Tether declined to seek MiCA authorization), and major exchanges delisted it for EEA users — handing the compliant European market to Circle (USDC and EURC) and MiCA-licensed newcomers. July 1, 2026 also marked the end of MiCA’s transitional period for crypto-asset service providers: the EU is now a fully licensed-only market.

- The euro stablecoin is finally being built — by banks. MiCA-compliant euro stablecoins are still tiny (roughly $674 million in aggregate as of early July 2026, but growing 128% year over year). The headline project is Qivalis, a consortium now spanning around a dozen major European banks — including BBVA, BNP Paribas, ING and UniCredit — building a MiCA-compliant euro stablecoin on Fireblocks infrastructure, regulated as a Dutch e-money institution, with reserves at least 40% in bank deposits and the rest in short-dated euro-area sovereign debt, targeting launch in the second half of 2026. It is explicitly framed as Europe’s answer to dollar-stablecoin dependence in digital settlement.

Hong Kong, the UK and the rest of the world

Hong Kong moved from framework to licenses fastest. The Stablecoins Ordinance took effect August 1, 2025, requiring an HKMA license to issue fiat-referenced stablecoins in or targeting Hong Kong, with full backing in high-quality liquid assets and par redemption. In the first licensing round, 36 entities applied and — on April 10, 2026 — exactly two licenses were granted: Anchorpoint Financial (a Standard Chartered / HKT / Animoca Brands joint venture) and HSBC, which is building on its tokenized-deposit experience. The message from the HKMA was unambiguous: this is a bank-grade regime, not a startup land-grab, and it positions Hong Kong as Asia’s regulated gateway — including for future offshore-CNH experimentation.

The United Kingdom is deliberately last but thorough. The FCA published its stablecoin issuance and custody rulebook on June 30, 2026; authorization applications open September 30, 2026, and the full mandatory regime takes effect October 25, 2027. Sterling stablecoins that become systemically important will be jointly regulated by the FCA and the Bank of England, and the Bank has consulted on transitional holding limits for systemic sterling stablecoins — a uniquely cautious feature that the industry is lobbying to relax.

Elsewhere: Japan has permitted bank- and trust-issued stablecoins since 2023 (with MUFG’s Progmat as the main platform); Singapore finalized its MAS stablecoin framework in 2023; the UAE’s regimes in Abu Dhabi and Dubai have attracted issuers targeting emerging-market corridors. The direction everywhere is the same: full reserves, redemption at par, licensed issuers, AML parity with banks.

The bottom line on regulation: the 2022 question — “will governments allow stablecoins?” — is answered. They will, enthusiastically, on the condition that stablecoins become what they always pretended to be: fully-reserved, redeemable, supervised digital dollars and euros. The trilemma’s fiat-backed corner is now the law of the land on three continents.

The best stablecoins in 2026

“Best” depends on what you need: deepest liquidity, strongest regulatory posture, on-chain transparency, or yield. Here is the field as of mid-2026 — the market totals roughly $303 billion, with the top two accounting for about 85% of it — followed by how to choose.

1. USDT (Tether) — ~$184 billion. The liquidity king, roughly 63% of the entire market. Deepest order books on every exchange, the default dollar in emerging markets, issued across many chains. Reserves (majority short-dated US Treasuries) are disclosed quarterly with attestations, but Tether remains outside the MiCA perimeter in Europe and has announced a separate US-market strategy for the GENIUS era. Best for: trading liquidity and global reach. Watch: how it lands US distribution once GENIUS enforcement begins.

2. USDC (Circle) — ~$73 billion. The compliance flagship. Monthly attested reserves held predominantly in a Treasury-only fund at BlackRock with custody at BNY Mellon; MiCA-authorized in Europe; issuer Circle went public on the NYSE in 2025. The default choice for US institutions, fintechs and DeFi blue chips. Best for: regulated flows and institutional treasury. Watch: reserve-chain banking concentration (the SVB lesson).

3. USDS / DAI (Sky, formerly MakerDAO) — ~$15 billion combined. The decentralized workhorse, over-collateralized by on-chain assets plus real-world collateral. Most exchanges completed the DAI→USDS conversion in April 2026. Best for: DeFi-native users who want to minimize single-issuer dependence. Watch: how an issuerless design fits (or doesn’t) into GENIUS-era distribution rules.

4. USDe (Ethena) — ~$4 billion. The synthetic dollar: fully collateralized, delta-hedged, yield-passing. Grew explosively in 2024–2025, then contracted as funding-rate yields compressed — a reminder that its economics are market-dependent. Best for: sophisticated on-chain users seeking yield who understand derivatives risk. Not a payment stablecoin, and not marketed as one.

5. PYUSD (PayPal/Paxos) — ~$3.4 billion. The fintech distribution play: a fully-reserved, Paxos-issued, NYDFS-supervised stablecoin wired into PayPal and Venmo’s hundreds of millions of accounts. Best for: consumer payments inside the PayPal ecosystem; a natural GENIUS-era winner.

6. USDG (Paxos / Global Dollar Network) — ~$2.4 billion. A consortium stablecoin (partners include Robinhood, Kraken and Galaxy) that shares reserve economics with distributors — the closest legal thing to “yield” under the no-interest rules, and a preview of how distribution wars will be fought.

7. RLUSD (Ripple) — ~$1.6 billion. Enterprise- and bank-oriented, NYDFS trust-company issuance, positioned for cross-border settlement alongside Ripple’s payments network and its 2026 MiCA authorization. Best for: institutional payment corridors.

8. USD1 (World Liberty Financial) — surged into the top ranks in 2026. Politically connected (the Trump-affiliated project), Treasury-backed reserves, aggressive exchange and liquidity integrations. Liquidity is real; the governance and concentration questions are too.

9. USDY (Ondo) — ~$1.3 billion. Tokenized-Treasury yield in transferable form; a bridge between stablecoins and tokenized money-market funds. Best for: non-US treasuries seeking on-chain dollar yield (US persons excluded).

10. EURC (Circle) — the leading euro stablecoin. Small next to the dollar giants but MiCA-authorized and growing fast as euro settlement moves on-chain; the incumbent that bank consortia like Qivalis are racing to challenge.

How to choose: for trading, liquidity wins — USDT globally, USDC on US venues. For corporate treasury and B2B settlement, regulatory posture and redemption rights win — USDC, PYUSD, RLUSD, or (in the EU) EURC and MiCA-licensed euro coins. For DeFi and censorship resistance, USDS/DAI. For yield, understand that a compliant payment stablecoin cannot pay you interest — yield lives in adjacent instruments (USDY, USDe, tokenized MMFs) with genuinely different risk profiles. And for anything at business scale: verify the issuer’s license and the redemption mechanics before you verify the APY.

Stablecoins and tokenization: why this matters beyond payments

Our own vantage point at Stobox is tokenized real-world assets, and from that seat stablecoins are not a product category — they are the settlement layer. A tokenized security, fund unit or revenue-share instrument only achieves atomic delivery-versus-payment if the cash leg is also on-chain. Every efficiency claim in tokenization — instant settlement, 24/7 markets, programmable distributions — quietly assumes a trustworthy stablecoin on the other side of the trade.

That is why the regulatory maturation described above matters far beyond crypto trading. A GENIUS-compliant dollar and a MiCA-licensed euro give issuers, transfer agents and investors a regulated cash instrument to settle against — the missing piece that let institutions dismiss tokenization for a decade. It is also why we build where the regulated money is converging: Stobox Compass issues security tokens primarily on Base, the chain where Coinbase’s ecosystem, USDC liquidity and bank experiments like JPMD are concentrating, and where our own STBU utility token now lives. Dividend distributions, subscription proceeds, redemption payouts — in a tokenized capital market, all of it moves as stablecoins.

If you are structuring an asset for tokenization, the stablecoin question shows up in concrete places: which stablecoin your investors can legally hold, which your paying agent will distribute, and which your jurisdiction’s regulator recognizes for settlement. Those answers now differ between the US, EU, UK and Hong Kong — which is exactly the kind of structuring question worth resolving before issuance, not after.

What comes next

Four things to watch through the rest of 2026:

- The GENIUS final rules (imminent) and the 120-day countdown. The moment the six agencies publish, the compliant-issuer race in the US formally begins, and offshore issuers’ US strategies stop being theoretical.

- The yield war. Whether CLARITY’s platform-yield ban survives the Senate will determine if stablecoin economics stay with issuers and distributors or shift toward holders — and how fast tokenized money-market funds cannibalize idle stablecoin balances.

- Bank money goes on-chain. Qivalis in Europe, Anchorpoint and HSBC in Hong Kong, deposit tokens like JPMD in the US: 2027’s stablecoin competitors are banks, and the line between “stablecoin” and “tokenized deposit” will blur.

- Consolidation of the long tail. Full-reserve regimes are expensive. Expect fewer, larger, better-audited stablecoins — and expect the surviving issuers to look increasingly like regulated financial institutions, because that is what they now are.

The triangle we started with still explains everything: the market chose collateral and capital efficiency, regulators wrote that choice into law, and decentralized designs continue as the important, smaller counterweight. Stablecoins began as crypto’s workaround for the banking system. In 2026, they are becoming part of it.

Frequently Asked Questions

What is a stablecoin in simple terms? A stablecoin is a digital token on a blockchain designed to always be worth a fixed amount of a real currency — usually exactly one US dollar. It combines the stable value of ordinary money with the speed, programmability and 24/7 availability of crypto.

What is the stablecoin trilemma? The stablecoin trilemma says a stablecoin design can achieve at most two of three properties: full collateral backing, capital efficiency, and decentralization. Fiat-backed coins (USDT, USDC) sacrifice decentralization; crypto-backed coins (DAI/USDS) sacrifice capital efficiency through over-collateralization; algorithmic coins sacrificed collateral — and mostly collapsed.

What are the three types of stablecoins? Fiat-backed (reserves of cash and Treasury bills held by an issuer), crypto-backed (over-collateralized by crypto assets locked in smart contracts), and algorithmic (peg maintained by supply mechanics rather than collateral). Fiat-backed designs represent roughly 95% of the market in 2026.

Why did TerraUSD (UST) collapse? UST was backed not by reserves but by an arbitrage loop with its sister token LUNA. When large withdrawals broke confidence in May 2022, the loop reversed: redeeming UST hyperinflated LUNA’s supply, LUNA’s price collapsed, and the “backing” evaporated — destroying roughly $60 billion in value within a week and triggering stablecoin legislation worldwide.

What does the GENIUS Act require? Signed July 18, 2025, the GENIUS Act allows only licensed “permitted payment stablecoin issuers” in the US, requires 1:1 reserves in cash and short-dated Treasuries, monthly examined reserve disclosures, full AML compliance, and gives holders first claim on reserves in insolvency. It also prohibits issuers from paying interest to holders. Final implementing rules from six federal agencies are due by July 18, 2026, with the regime fully effective by early 2027.

What is the difference between the GENIUS Act and the CLARITY Act? The GENIUS Act is law and governs stablecoin issuance specifically. The CLARITY Act is broader market-structure legislation — dividing SEC and CFTC jurisdiction over digital assets and regulating exchanges and brokers. As of mid-July 2026 CLARITY has passed the House and Senate Banking Committee and awaits a Senate floor vote, with stablecoin yield rules among the final sticking points.

Are stablecoins legal in Europe? Yes, under MiCA. Fiat-referencing stablecoins may only be offered by EU-authorized credit or e-money institutions with fully backed, redeemable-at-par reserves. USDT is not MiCA-authorized and was delisted from regulated EEA venues, while USDC, EURC and newly licensed euro stablecoins operate compliantly. A consortium of major European banks (Qivalis) plans a MiCA-compliant euro stablecoin in late 2026.

Which stablecoin is the safest? There is no single answer, but for most users the safest options are large, fully-reserved, regulated issuers with attested Treasury-backed reserves and clear redemption rights — USDC is the usual institutional benchmark, with PYUSD and RLUSD in the same regulated tier, and USDT offering the deepest liquidity with a different regulatory profile. Safety also depends on custody: how you hold a stablecoin matters as much as who issues it.

Can stablecoins pay interest? Under the GENIUS Act, US-regulated payment stablecoin issuers cannot pay holders interest, and pending CLARITY Act language may extend that ban to platforms. Yield therefore lives in adjacent instruments — tokenized money-market funds, tokenized Treasuries like USDY, or synthetic dollars like USDe — which carry different risks and regulatory treatment than payment stablecoins.

How big is the stablecoin market in 2026? Roughly $303 billion in total circulating value as of mid-July 2026, with USDT ($184B) and USDC ($73B) accounting for about 85% of it. Euro stablecoins remain small — under $1 billion combined — but are the fastest-growing regulated segment.

What role do stablecoins play in real-world asset tokenization? They are the cash leg. When a tokenized security or fund unit trades, settles, or pays a distribution, stablecoins let the money move on the same rails as the asset — enabling atomic delivery-versus-payment, 24/7 settlement and programmable payouts. Regulated stablecoins are the piece that makes institutional tokenization operationally complete.

Are stablecoins a good investment? Stablecoins are not designed to appreciate — they are cash instruments, and holding them is like holding dollars, with issuer and custody risk but no upside. They are working capital for trading, payments and settlement, not an investment. Anything promising high “stablecoin yield” is compensating you for risks that deserve careful reading. This is general information, not investment advice.

Put stablecoins to work in a tokenization strategy

If you are exploring tokenization — of real estate, a fund, private credit, equity or another asset — the stablecoin layer is one of the structural decisions that determines whether your project settles efficiently and stays compliant across jurisdictions. Stobox has built compliance-first tokenization infrastructure since 2018, and settlement design is part of every engagement.

Two ways to go deeper:

- Assess your asset with Stobox Compass — the guided workflow that takes a tokenization project from readiness assessment through structuring to issuance, including the settlement and jurisdiction questions raised in this guide.

- Book a discovery call with our team to discuss your specific asset, jurisdiction and settlement requirements directly.